Spring Budget 2023: The Pensions Perspective and how it impacts you.

Originally published March 24th 2023

The Chancellor was still speaking at the dispatch box, delivery the eagerly anticipated Spring Budget as the first of many e-mails, text and WhatsApp messages began arriving in my inbox and phone from eager clients.

“What does this mean for me?”, “Shall I start funding my pension again now?” and “Will I lose my protected tax-free cash?”

Some messages turned to anger at having forfeit many years of making contributions, others predicted that a future Government would repeal the proposed changes.

From my own perspective, as interesting as the new planning opportunities created are, what is perhaps of equal interest is the behavioral-finance angle. Last year, 2022 was a year during which our brains were attacked from so many different angles: – the War in the Ukraine, rising inflation and the cost-of-living crisis, successive interest rate hikes, four chancellors, three Prime Ministers, the death of a beloved monarch and of course the financial turmoil wrought by the ill-fated 45-day government of Liz Truss.

We should all be forgiven for thinking that the UK was on its knees and that the Treasury would be shaking out all the tools in its toolbox, including punitive pension changes, to stave off the expected recession.

Naturally therefore the media began making predictions and clients began to become unnerved even to the point of wanting to take decisive action NOW based on mere speculation, so compelling did the arguments sound. Here’s a summary of the most common predictions I read or heard during 2022:

The removal of Pension Commencement Lump Sum (known as tax free cash until 2006)

The lowering of the Lifetime Allowance (LTA)

Increases to the Lifetime Allowance Charge

Reduction to pension tax relief

Removal of the Inheritance Tax advantages of pension funds

Remembering that ‘bad news sells’, there should be no surprise that the above all have very negative connotations. However, whilst such predictions might sell newspapers they ignore two very fundamental issues:

Since, 2016 when the Lifetime Allowance cap fell to £1.25m my colleagues and I have been quietly saying that if the LTA was going to go anywhere it would be raised or removed because it had begun to impact the demographic it was never intended to touch – doctors, nurses, teachers, police officers and other civil servants. To say nothing of the fact that it wasn’t necessary to continue with both annual allowance (accumulation) and LTA (decumulation) restrictions.

The lifting of COVID restrictions has revealed serious shortcomings in the UK labour market with huge shortages in most industries, particularly in health and social care.

Should we be that surprised therefore that we saw a budget aimed specifically at addressing these problems? The softening of pension restrictions to get the 50-somethings back into the work force whilst also helping younger generations into work with much needed support for childcare.

It all makes sense now with hindsight.

But this is not intended to be an ‘I told you so’ moment, but rather a cautionary reminder to ignore the noise and speculation and to focus on what we can control.

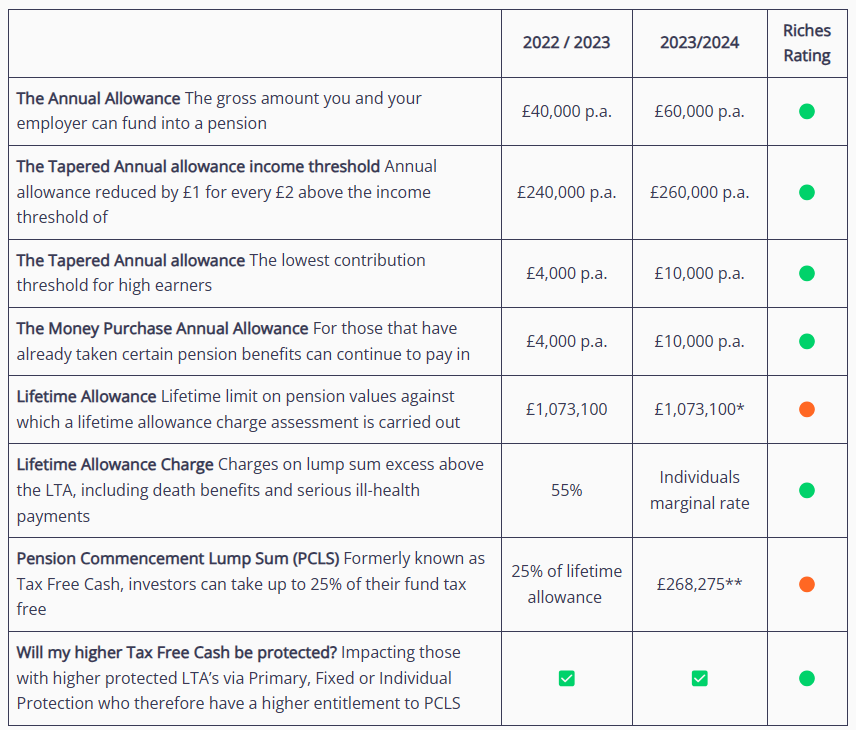

So, let’s have a quick look at what has changed: (I accept the jargon is like a foreign language to you, which is why you’ve got us to help!)

*LTA Charge removed from April 2023 and LTA completely abolished from April 2024.

**The amount of money you can take from your pension fund has been restricted to 25% of today’s LTA (£268,275) or your own protected LTA if higher. It is unclear whether this LTA level will remain as a reference point or be index linked – hence the neutral rating.

Summary

So, pension funding is now back on the agenda for both high earners and / or those who stopped funding due to LTA considerations and we will be picking this up with you within the normal cycle of annual planning meetings.

If you do have specific questions as to how these changes will impact on your personal situation, then please contact your Capital adviser.

Charles’ Top Tips

July of 2023 will mark 23 years of private client advising for me, in all that time I have probably seen pensions legislation change some 30 times and I imagine we will see it change 30 more times before I eventually hang up my calculator.

By far the biggest piece of advice I can give anyone is that we can only play with what is in front of us, never try to second guess what the future holds and never, ever allow the tax-tail to wag the decision dog.